Project Cost Management: Definition, Process, Challenges (With Template)

Learn the essentials of project cost management! This beginner's guide covers planning, estimating, budgeting, and controlling project costs to prevent overruns

What is Project Cost Management

Project cost management is the process of planning, estimating, budgeting, and controlling a project’s costs. It helps the project manager forecast expenses, allocate resources effectively, and monitor spending throughout the project to keep everything within the approved budget and avoid cost overruns.

Why is Project Cost Management So Important?

Let’s be blunt: money matters. In the project world, failing to manage costs effectively can lead to a cascade of problems, and project cost management helps:

- Preventing Budget Overruns: This is the most obvious benefit. Solid project cost management helps you anticipate expenses and keep spending aligned with the plan, preventing nasty surprises and frantic searches for extra funding. Without it, you risk running out of money before the project is finished.

- Improving Decision-Making: Accurate cost data empowers project managers and stakeholders to make informed decisions. Should we pursue a specific feature? Can we afford a particular resource? Effective project cost management provides the financial context needed to answer these questions confidently.

- Increasing Stakeholder Confidence: Nothing builds trust like delivering a project on budget. Good project cost management demonstrates competence, fiscal responsibility, and reliable execution, keeping stakeholders happy and supportive. Conversely, poor project cost management erodes trust quickly.

- Ensuring Project Profitability & ROI: For many projects, especially commercial ones, staying within budget is directly linked to profitability and achieving the desired Return on Investment (ROI). Diligent project cost management safeguards the project’s financial viability.

- Better Resource Allocation: Understanding costs helps optimize resource planning. Knowing the cost implications of using certain team members, equipment, or materials allows for more strategic allocation, ensuring resources are used efficiently. This is a critical part of overall resource management.

In essence, project cost management acts as the financial compass for your project, guiding it safely through potentially turbulent economic waters. It’s an indispensable part of holistic project management.

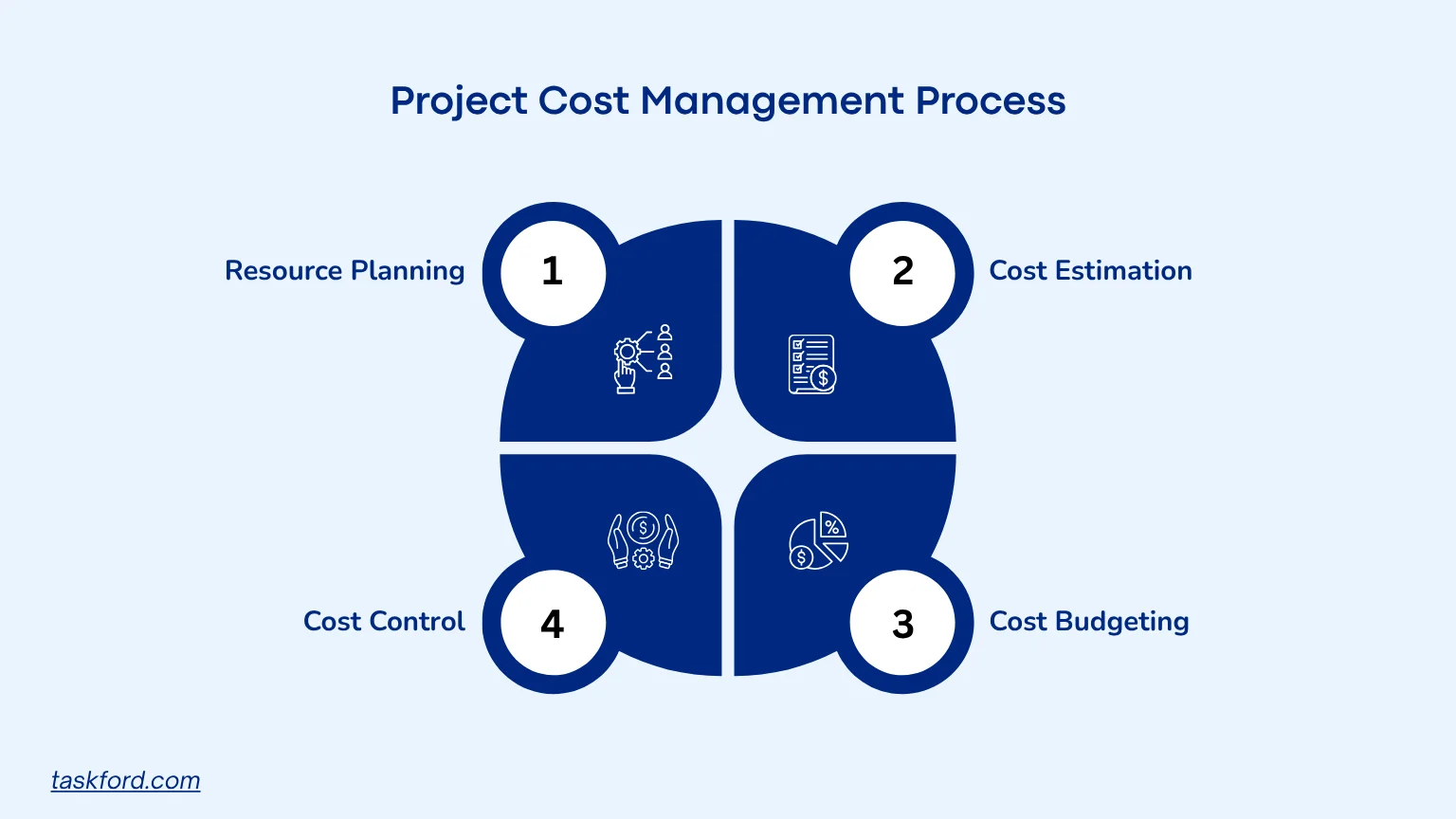

The Core Process of Project Cost Management

According to established frameworks like the Project Management Institute’s (PMI) PMBOK® Guide, project cost management typically involves four key process groups. Let’s break them down:

1. Project Resource Planning

Resource planning involves identifying everything needed to complete the project, including people, equipment, and materials. This step takes place early in the project, before execution begins.

Project managers typically start with a work breakdown structure (WBS) and analyze each task to determine:

- What skills and roles are required

- How many people are needed

- What equipment or materials are necessary

This detailed, task-level approach helps build a complete inventory of resources, which becomes the foundation for accurate cost estimation.

Best practices for resource planning:

- Use historical data from past projects when available

- Collaborate with leaders and team members

- Consider timing and availability of resources

- Account for real-world constraints, such as hiring needs or training gaps

2. Cost Estimation

Cost estimation is the process of calculating the total cost of all required resources. It relies on inputs such as resource requirements, pricing, project duration, assumptions, risks, and historical benchmarks.

Because accuracy is critical, project managers must consider multiple factors, including:

- Fixed vs. variable costs

- Overhead expenses

- Inflation and time value of money

Different estimation methods can be used depending on the project:

- Analogous estimation: Using historical data from similar past projects. Quick but less accurate. Relies on good record-keeping from previous project cost management efforts.

- Parametric models or PERT: Use mathematical formulas for forecasting. More accurate if the underlying data and model are solid.

- Top-down approach: Based on overall project experience and assumptions.

- Bottom-up approach: Estimating the cost of individual work packages or tasks and rolling them up to get a project total. Most accurate but also most time-consuming. Requires detailed task management.

This relies heavily on the scope baseline, project schedule, resource planning details (who/what is needed), risk register, and historical data. Accurate project cost management hinges on quality inputs.

3. Cost Budgeting

Cost budgeting involves allocating estimated costs to specific tasks or phases over a defined timeline. This step transforms estimates into a structured budget and establishes a cost baseline for measuring performance.

Budgets typically include:

- Allocated costs for tasks or project phases

- Time-based distribution of spending

- Contingency reserves for unexpected expenses

By breaking down the total cost into smaller, time-bound budgets, project managers can track progress more effectively and make better financial decisions throughout the project.

Budgeting also ensures that spending aligns with available funding and expected cash flow, especially in long-term projects.

4. Cost Control

Cost control is the ongoing process of monitoring the project’s status to update the project costs and managing changes to the cost baseline. It’s about keeping the financial train on the tracks throughout the project. This is where active project cost management happens daily.

- Key Activities:

- Monitoring Performance: Tracking actual costs incurred against the work being done. Accurate time tracking and timesheet data are invaluable here.

- Variance Analysis: Comparing planned costs (baseline) to actual costs and identifying differences (variances). Is the project over or under budget? Why? This is core to project cost management.

- Earned Value Management (EVM): A powerful technique that integrates scope, schedule, and cost performance. Key metrics include:

- Planned Value (PV): Budgeted cost for work scheduled.

- Earned Value (EV): Budgeted cost for work actually completed.

- Actual Cost (AC): Actual cost incurred for work completed.

- Schedule Variance (SV = EV - PV): Are we ahead or behind schedule?

- Cost Variance (CV = EV - AC): Are we over or under budget?

- Schedule Performance Index (SPI = EV / PV): Schedule efficiency.

- Cost Performance Index (CPI = EV / AC): Cost efficiency. (For a deeper dive into EVM, resources like the PMI website are excellent). Effective project cost management often utilizes EVM.

- Forecasting: Predicting future project performance based on current data (e.g., Estimate at Completion - EAC).

Effective cost control provides transparency and enables quick, informed decisions—especially in complex projects with many moving parts.

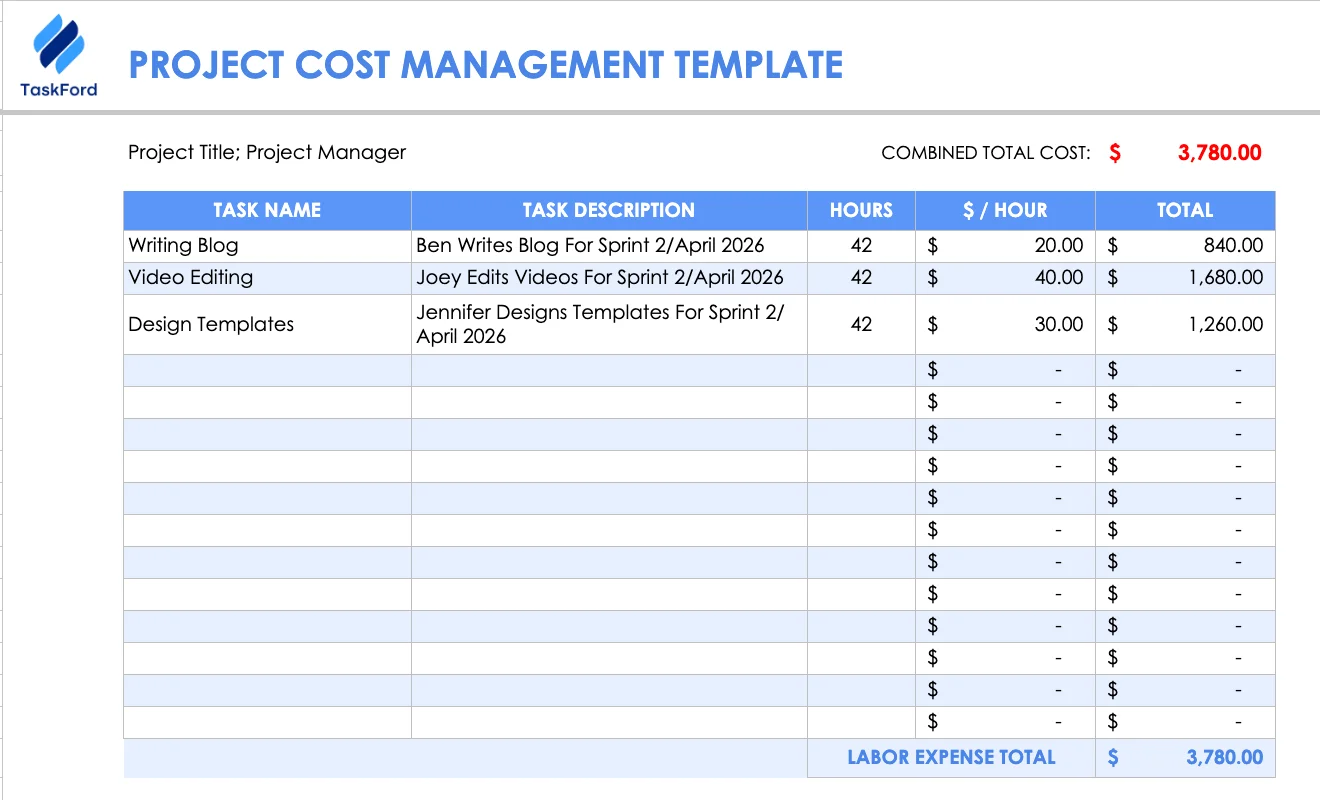

Project Cost Management Template

This basic project cost management template helps project managers calculate the labor cost amongst project team members. It shows the number of tasks, price per task, and total cost. The template will then automatically calculate total cost per member and display the total estimated project cost at the top of the template.

Common Challenges in Project Cost Management (and How to Dodge Them)

Even with the best intentions, project cost management can hit roadblocks. Here are common culprits and potential solutions:

Inaccurate Initial Estimates: This occurs when projected costs don’t reflect reality, often leading to budget overruns later in the project. It is typically caused by optimism bias, unclear scope, or a lack of reliable historical data.

- Solution: Use a mix of estimation techniques, break work into smaller tasks with a WBS, involve experienced team members, and include contingency buffers based on identified risks.

Scope Creep: This happens when the project scope expands without proper control, increasing costs without corresponding budget adjustments. It is usually caused by uncontrolled changes or unclear initial requirements.

- Solution: Clearly define the scope from the beginning, implement a formal change control process, and assess the cost and timeline impact before approving any changes.

Poor Risk Management: When risks are not properly identified or planned for, unexpected issues can lead to additional costs. This is often caused by insufficient risk analysis or lack of ongoing risk monitoring.

- Solution: Identify and evaluate risks early, prioritize them based on impact, and allocate contingency reserves to handle potential uncertainties.

Lack of Real-Time Visibility: Without up-to-date cost data, it becomes difficult to track spending and respond to issues quickly. This is commonly caused by outdated tools, infrequent reporting, or siloed information.

- Solution: Use integrated project management tools, track expenses and resource usage in real time, and establish consistent reporting practices to improve visibility and control.

Best Practices for Effective Project Cost Management

To keep projects on budget and avoid financial surprises, teams should follow a set of proven best practices that improve accuracy, control, and decision-making throughout the project lifecycle.

- Define a clear scope from the start: A well-defined scope reduces uncertainty and helps prevent unexpected costs caused by misalignment or scope creep.

- Break work into a detailed WBS: Smaller tasks make it easier to estimate costs accurately, assign resources, and track progress throughout the project.

- Use multiple estimation methods: Combine approaches like top-down, bottom-up, and historical data to improve the reliability of your cost estimates.

- Track costs regularly: Monitor actual spending against the budget in real time to identify variances early and take corrective action quickly.

- Implement strong change control: Ensure all changes are reviewed and approved with a clear understanding of their impact on cost and timeline.

Following these best practices helps create a more disciplined and proactive approach to project cost management, ultimately increasing the chances of delivering projects on time and within budget.

Conclusion: Taking Control of Your Project Finances

Project cost management is not just about tracking expenses. It is about planning ahead, making informed decisions, and staying in control throughout the project. By following a clear process that includes resource planning, estimation, budgeting, and cost control, teams can reduce uncertainty and manage their budgets more effectively.

Challenges like inaccurate estimates, scope creep, and limited visibility are common, but they can be managed with the right approach. With clear processes, regular tracking, and the right tools, teams can stay on budget and avoid surprises. In the end, strong cost management helps projects run more smoothly and builds greater confidence with stakeholders.

Frequently Asked Questions (FAQs)

What is project cost management?

Project cost management is the process of planning, estimating, budgeting, and controlling costs to keep a project within its approved budget.

What are the 4 types of costs?

The four main types of costs are fixed costs, variable costs, direct costs, and indirect costs. Fixed costs stay the same regardless of activity, variable costs change based on usage, direct costs are tied to specific tasks, and indirect costs support overall operations.

Why is cost estimation important?

Cost estimation helps teams forecast expenses and plan budgets before work begins. More accurate estimates reduce the risk of going over budget and support better decision-making.

How do you control project costs?

Project costs are controlled by tracking actual spending against the budget, identifying any differences, and making adjustments such as changing scope, reallocating resources, or updating plans.

What tools can help with project cost management?

Project management tools help teams track budgets, monitor resource usage, and get real-time visibility into costs. This makes it easier to stay on budget and respond quickly to changes.

Subscribe for Expert Tips

Unlock expert insights and stay ahead with TaskFord. Sign up now to receive valuable tips, strategies, and updates directly in your inbox.